Editor's Note: Driven by multiple factors such as the decline in global copper mine output growth, tightening supply of copper concentrates, and rising expectations for production cuts at smelters, coupled with sustained growth in copper demand from sectors like NEVs and power grid investments, highlighting the resilience of demand, as well as market concerns triggered by the US's proposed tariff hikes on imported copper, leading to stockpiling, and exacerbated geopolitical conflicts in the DRC, copper prices ultimately closed the first half of the year with gains. LME copper saw a 12.66% increase in its semi-annual line, while SHFE copper rose by 8.22%, and SMM #1 copper cathode recorded a cumulative increase of 8.4% in the first half. Now, as the second half unfolds, whether these factors that drove copper prices higher in the first half will continue to play a role has become a focal point of market attention! Whether copper prices can sustain the upward momentum of the first half remains to be seen over time.

》Click to view SMM Futures Data Dashboard

Spot Market

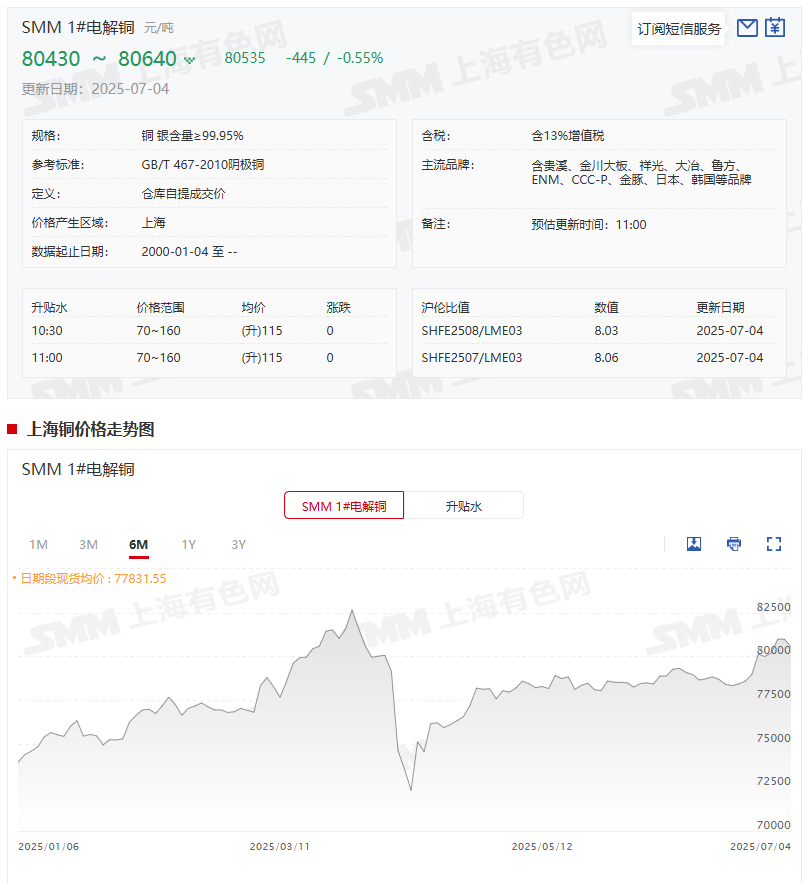

Spot prices of copper cathode rose by 4% YoY in the first half

》Click to view SMM spot prices of metal copper

》Subscribe to view historical price trends of SMM metal spot prices

Regarding spot prices:According to SMM quotes, the daily average price of SMM #1 copper cathode in the first half of the year was 77,657.65 yuan/mt, compared to 74,552.86 yuan/mt in the first half of 2024, an increase of 3,104.79 yuan/mt or 4%. Since entering July 2025, SMM #1 copper cathode prices have fluctuated, with the overall center of its average price slightly moving upwards. On July 4, the average price was 80,535 yuan/mt, compared to 79,990 yuan/mt on June 30, an increase of 545 yuan/mt or 0.68%.

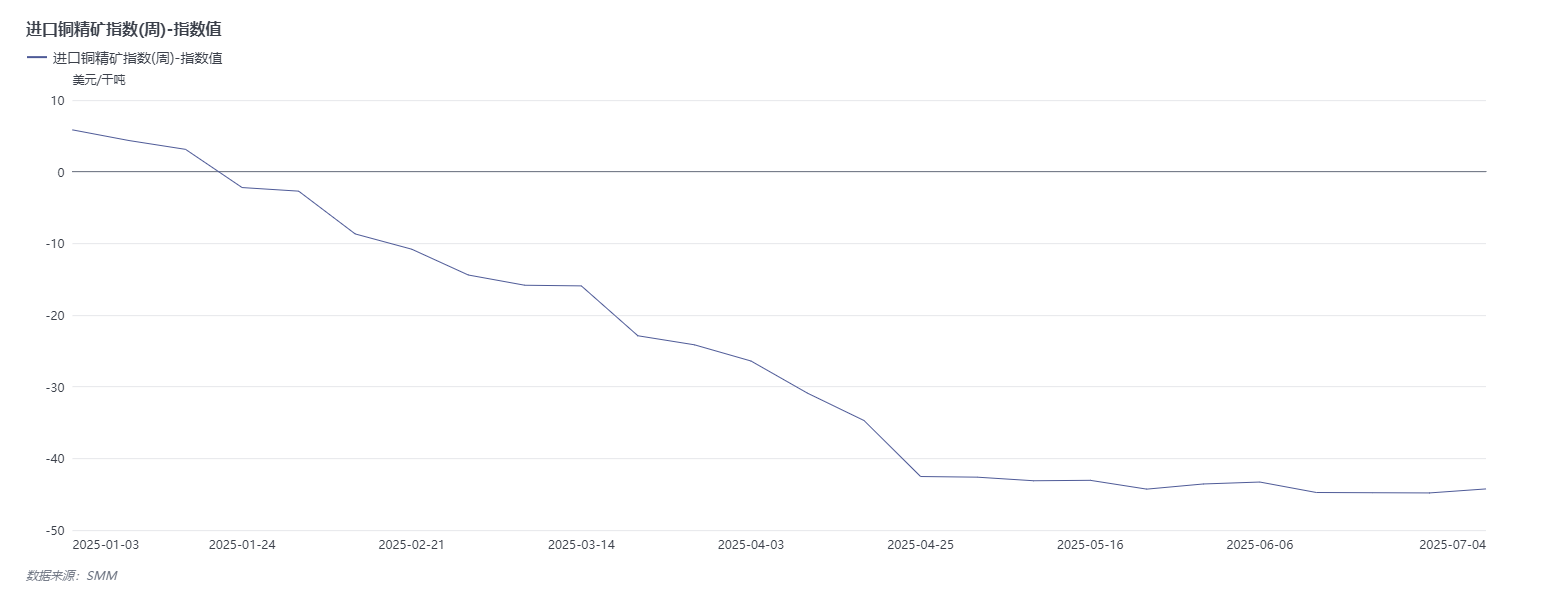

The SMM Imported Copper Concentrate Index (weekly) showed an overall downward trend in the first half of the year

》Click to view SMM Metal Industry Chain Data Terminal

Looking back at the first half of the year, the trend of the SMM Imported Copper Concentrate Index (weekly) was closely related to market concerns about the shortage of copper concentrate supply, showing an overall downward trend. In the week of January 3, the index stood at $5.85/dmt; by the week of June 27, it had dropped to -$44.81/dmt, a cumulative decrease of $50.66/dmt over half a year, visually reflecting the continued intensification of the tight supply situation of copper concentrates. However, recently, the index has shown signs of stabilizing and rebounding. As of the week of July 4, the SMM Imported Copper Concentrate Index (weekly) was -$44.25/dmt, an increase of $0.56/dmt from the previous week.

From an industry perspective, according to previous SMM insights, the TC/RC negotiation results between Antofagasta and Chinese smelters for mid-2025 were finalised at $0.0/dmt and $0.0/lb.

Copper cathode production in H1 increased by 674,700 mt YoY up 11.4% YoY

Production: Halfway through 2025, domestic copper cathode production has reached new heights. According to SMM, from January to June 2025, the cumulative production of copper cathode increased by 674,700 mt, a rise of 11.40%, showing a strong growth trend. So, why did domestic copper cathode production see such an explosive increase in H1? This is closely related to the release of domestic smelting capacity. Since H2 2024, new smelters have been put into operation, with most of the new capacity coming online in Q4 2024 and Q1 2025. In H1 2025, the capacity utilization rates of these newly commissioned enterprises continued to rise, with some even reaching full production, directly driving the steady increase in domestic copper cathode production.》Click for more details

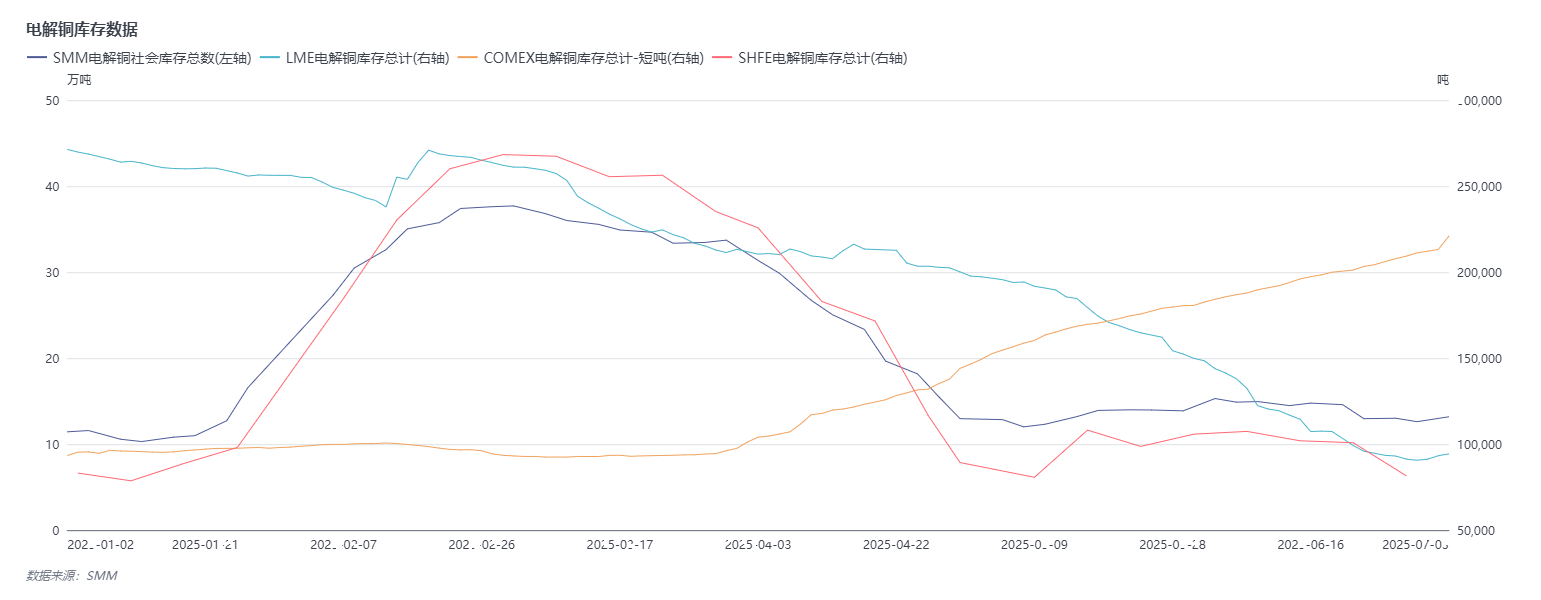

LME copper inventories fell by nearly 70% while COMEX copper inventories surged

》Click to view SMM Metal Industry Chain Database

Inventory: According to SMM's data on copper inventories in major regions across the country, the inventory trend in H1 2025 showed certain fluctuations. Entering 2025, as of January 2 (Thursday), the copper inventory in major regions was 114,300 mt. Subsequently, the inventory showed an upward trend, peaking at 377,000 mt on March 3. However, after reaching this peak, the overall inventory entered a destocking phase, falling to 126,100 mt by June 30 (Monday), an increase of 11,800 mt from the beginning of the year. Notably, the current copper inventory in major regions remains around 130,000 mt, significantly lower compared to the approximately 400,000 mt level at the same period last year. This low inventory level also reflects some changes in the supply-demand relationship in the copper market in H1.

From the perspective of LME copper inventory data, the LME copper inventory on June 30 was 90,625 mt, down 180,725 mt from 271,350 mt on January 2, a decrease of 66.6%.

As for COMEX copper inventory data: The COMEX copper inventory on June 30 was 211,209 short tons, up 117,837 short tons from 93,372 short tons on January 2, an increase of 126.2%.

Outlook

►Macro front

Domestic: The market has strong expectations for favourable macro conditions, with attention on the policy signals to be released at the upcoming important meeting. Fiscal Policy: In H2, the focus of fiscal policy will center on accelerating the implementation of existing policies and timely introduction of incremental policies. With the concentrated issuance of ultra-long-term special treasury bonds and special-purpose bonds in Q3, fiscal expenditures will maintain their intensity. Concurrently, additional ultra-long-term special treasury bonds may be issued to further support key areas such as the program of large-scale equipment upgrades and consumer goods trade-ins and the implementation of major national strategies and build up security capacity in key areas, while extending trade-in policies to the service consumption sector. New-type policy-based financial instruments may also be established to guide more private capital into infrastructure construction, as well as priority sectors like technology, foreign trade, and consumption, thereby bolstering domestic economic growth. Monetary Policy: The market widely anticipates further cuts in the LPR and reserve requirement ratio (RRR) in H2. Capital Market Policy: Capital market reforms are expected to deepen further to attract more medium and long-term funds. Consumption Policy: H1 saw significant efforts to stimulate consumption, while H2 policies may focus more on scenario innovation in cultural tourism, sports, and health consumption, optimizing measures like tax refunds for overseas visitors to enhance convenience, aiming to unlock consumption potential across multiple dimensions. Meanwhile, fiscal funds may support livelihood areas such as childbirth, employment, and service consumption, thereby boosting residents' medium and long-term consumption willingness.

Overseas Developments: US Fed Policy: The stronger-than-expected June non-farm payrolls data extended the Fed's wait-and-see period, with markets nearly abandoning bets on a July interest rate cut. Currently, the probability of a September rate cut is estimated at around 70%. If the Fed cuts rates as expected and US policies effectively prop up the economy, copper prices will find support; however, a sharper-than-anticipated global economic downturn would dampen copper demand. Tariff Policy: The timing and rate of the US Section 232 tariffs on copper imports will be key variables affecting copper price trends. If a 25% tariff is imposed before September, US copper inventories are expected to rise in Q3 while declining elsewhere. Post-implementation, US stockpiling demand would ease, likely leading to reduced US inventories and increased inventories in other regions in Q4. If the tariff is delayed beyond expectations, US imports may continue into Q4, further tightening non-US markets and supporting copper prices. Caution is warranted against potential volatility in US tariff policies disrupting copper prices.

Fundamentals

Supply Side: Looking ahead, global incremental supply of copper concentrates will remain relatively limited, primarily relying on expansion projects at existing copper mines. Few world-class new copper mine projects are coming online, and their contributions will be marginal, insufficient to alleviate supply pressures. Moreover, large-scale developable copper mine projects have become increasingly scarce globally. As a result, the shortage of copper concentrates continues to intensify, and the undersupply situation in the short term is difficult to reverse. Given that market concerns about the supply of copper concentrates are unlikely to dissipate in the short term, it is expected that this will provide strong support for copper prices from the raw material side. Currently, there is a supply mismatch issue with copper cathode. The US over-imported copper cathode in the first half of the year, and inventories in non-US regions are at low levels. If this situation persists, it will support copper prices; if the supply mismatch issue is resolved due to factors such as the implementation of tariffs, the upside room for copper prices will be limited.

On the demand side, although power grid demand may remain strong, considering the pressure on home appliance exports brought by tariffs and the impact of factors such as "anti-cut-throat competition," and given that global consumption growth is expected to be lower than last year's projections, copper demand may weaken marginally in the second half of the year, which will have a certain inhibitory effect on copper prices.

From the inventory perspective, current domestic copper inventories and LME copper inventories are at low levels, providing support for copper prices from the low inventory side. It is worth noting that current LME inventories are at historically low levels, making it highly prone to squeeze behavior, which will support copper prices. However, with changes in US tariff policies and adjustments in the global supply-demand relationship, inventory situations may change, thereby affecting copper prices.

In summary, the market has strong expectations for increased domestic policy support, which is expected to bring a macroeconomic boost to copper prices; whether the US Fed can cut interest rates as scheduled, market concerns about the Fed's independence, trade negotiations between the US and multiple countries, and uncertainties surrounding US tariffs may repeatedly disturb copper prices. Fundamentals side, although there is a possibility of marginal weakening in overall copper demand growth in the second half of the year, the support for copper prices from the supply-side shortage is stronger, enabling copper prices to still receive relatively strong fundamental support in the second half of the year.

Institutional Voices

On July 3 (Thursday), a report released by UBS showed that it raised its copper price forecasts for 2025 and 2026 by 7% and 4%, respectively, to $4.24 per pound and $4.68 per pound, reversing its previously more cautious demand outlook as the significant impact of tariff uncertainties has dissipated. Although tariff uncertainties may lead to a reduction in end-user demand, UBS's base case scenario forecasts that demand will return to trend levels within the next 12 months. The recovery of traditional end-use markets such as Europe and the US will support copper prices, with demand in these markets supported by long-term drivers such as restocking and electrification, German fiscal policy, defense, and AI industries. Supported by favorable supply-side dynamics and long-term demand drivers, UBS maintains a relatively optimistic view on copper prices.

Goldman Sachs expects that there is upside risk for LME copper prices in August, with a forecasted price of $10,050/mt. Goldman Sachs has previously raised its forecast for LME copper prices in H2 2025 to an average of $9,890/mt, up from the prior $9,140/mt, and projects copper prices will fall to $9,700/mt by December this year. Copper prices are expected to peak at $10,050/mt in 2025. The 2026 annual average price is forecast at $10,000/mt (revised down from $10,170/mt previously), with prices projected to reach $10,350/mt by December 2026.

Commerzbank expects copper prices to reach $9,500/mt by year-end.

CITIC Securities' research report states that copper prices have recently fluctuated upward, with market views on subsequent price trends diverging. From a commodity perspective, production guidance and CAPEX expansion for upstream refined copper mines remain extremely limited, while TC/RC fees continue to drop sharply. The global refined copper market maintains an overall tight balance. Additionally, China's "steady growth" and the US's "soft landing" economy underpin copper price floors. Current market prices are relatively reasonable, but further upward momentum requires stronger domestic macro policy support and stabilization of overseas economies as the industry awaits a new cycle. Elevated inflation expectations, interest rate cut expectations, and a slight pullback in the US dollar index are all anticipated to support copper prices in sustaining their current upward trajectory. CITIC Securities maintains its forecast for copper prices to rise to $10,000-$11,000/mt in H2 2025, while remaining cautious about potential disruptions from unexpected "reciprocal tariff" issues in July.

Recommended readings:

》Why China's H1 copper cathode production surged 674,700 mt!!! [SMM Analysis]